and Super is not super as again it takes many years depending on earning rates, how must you invest & yes the net returns & finally will Government change the rules because they can.

Read more: Is there are better alternative to saving 600K in super or rental property?

Hi I quickly wanted to wish you a Merry Christmas.

Stay well and enjoy the holidays.

Looking forward to catching up in the New Year.

John

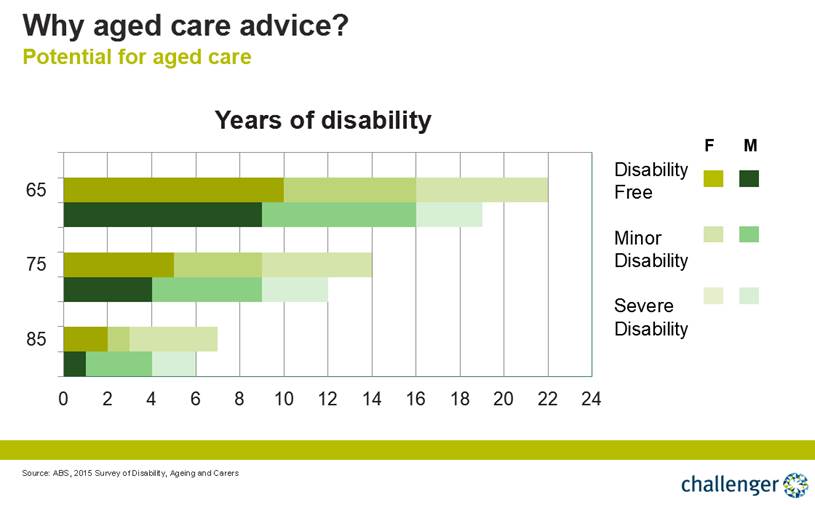

Read more: you’ll eventually spend more in dealing with the consequences of poor health

as only in this last 1 hour i chatted with a man who sadly lost his wife earlier this year & still not resolved with the Public trustee

We are currently in the actioning of a financial plan which means to act in his best interest we need to know exactly what the client has today.

He does have a very good Income protection & life cover placed by another adviser.

All very good & it retains cover when cashflow is sad during the not uncommon months of unemployment.

However it is drawn 90% from his equity in his super which means a lot less in retirement capital.

>

> Hi John,

>

> > Some exciting news. L***** age pension has finally been approved!

>

> Not only will he be receiving payments from 14th September, but payment has been backdated to January, when the original claim was submitted (and which Centrelink lost)

Read more: We’ll have to shout you a bottle (or three) of red wine, or a bottle of Scotch! >

RG 175.267 Section 961B(2) provides a ‘safe harbour’ for advice providers.

If an advice provider can show that they have taken the steps in s961B(2),

they are considered to have complied with the best interests duty.

Book a free 10 minute call and learn insights from our work with clients over the past 36 years

RG 175.268 The safe harbour requires an advice provider to:

(a)identify the objectives, financial situation and needs of the client that were disclosed by the client through instructions;

(b)identify

:(i)the subject matter of the advice sought by the client (whether explicitly or implicitly);

and

( ii)the objectives, financial situation and needs of the client that would reasonably be considered relevant to advice sought on that subject matter (client’s relevant circumstances);

(c)if it is reasonably apparent that information relating to the client’s relevant circumstances is incomplete or inaccurate, make reasonable inquiries to obtain complete and accurate information

Book a free 10 minute call and learn insights from our work with clients over the past 36 years

#financialadviser #financialadvisor #financialwellbeing #financialplanner #financialfitness

Contact today if you want to move forward & not stay where you are.

John

Get Sorted

“Retirement This is a topic that bamboozles many adults, with 13 per cent unsure of what their main sources of income would be in retirement, and another 30 per cent having no idea how much money they’d need to saved or invested to have a comfortable retirement.”

so we read from an online NZ Stuff article titled “Third of adults would fail school money course for teenagers”

and it continues with “About a third of adults would benefit from going back to school to do a new taxpayer-funded money management NCEA course designed for their children.

The Sorted for Schools NCEA course for children aged 14-17 was created by the Commission for Financial Capability (CFFC), but its research indicates many adults lack the money management, saving, debt, goal setting, insurance, investing, KiwiSaver and retirement skills it's designed to teach to secondary school children”.

The results in Australia are no different when 76% of retirees require some form of government support.

In 2020 this has been demonstrated with 2 million requesting funds for their super as they were not prepared for the inevitable “Rainy Day”.

Now is the time to take a 5 min financial check up & ‘Get Sorted’.

John McAuliffe

John Michael McAuliffe AFA, DipFp., BSc., DipTeach.